How To Invest Under Age 18

by Emmanuel Modu, Author of TeenVestor: The Practical Investment Guide for Teens and Their Parents

Updated: July 7, 2025

The most commonly asked question by teens who visit this site is “how old do I have to be to invest in stocks?”. In this article, we tell you how to invest in stocks and other financial assets under 18 with the help of your parents (through custodial accounts).

Advantages of Learning to Invest as a Teenager

What are the advantages of investing under 18? First, you will get ahead of all your peers. While your friends worry about affording the latest device or fashion, you will be investing in their manufacturers. While your classmates set aside their holiday gift money for a new game system, you will be stashing money in financial assets like stock and mutual funds.

Investment principles learned early will stay with you forever. When you appreciate how money grows by earning interest on interest (also known as compounding) and investing long-term in stocks and mutual funds, you will realize that a bit of money invested today can produce much more tomorrow.

Two very important factors that determine how teenagers under 18 years old (or minors) can invest are:

Teens under 18 can’t invest on their own — they must do so through custodial accounts supervised by adults; and

Teens generally have very little money so it limits the variety of investments they can make; (for example, they generally can’t invest in mutual funds because many mutual funds require huge investments of thousands of dollars).

What Teens Will Learn about Investing

This article explains how to invest as a teenager by addressing the above mentioned obstacles.

Along the way, we discuss custodial accounts for minors and affordable investments, including stocks, exchange-traded funds (ETFs), United States Savings Bonds, and Certificates of Deposits (CDs). In addition, it briefly addresses the issue of teen investors and taxes — a subject often ignored by minors investing in the stock market and other financial assets.

Remember, we are not financial advisors, so you should consult your parents or professional money advisors about investing in any assets. All investments involve a certain amount of risk that should not be ignored.

Before we get into investing under 18, you should consider registering for the TeenVestor Stock Certification Course.

As you are preparing to invest as a teenager, you should also check out our article on 7 Steps to Investing as a Teenager, which outlines the following steps in your journey to becoming a prudent investor:

Gain Basic Knowledge -- go to sites that specialize in teaching teens about stocks basics (see: www.teenvestor.com/teen-websites)

Stick to Your Interests at the Beginning -- looking for companies that suit your interest will keep you engaged; later, you can expand your investment universe.

Find out Exactly What Companies Do -- you should know the business in which your company of interest is engaged.

Get Basic/Simple Financial Data -- understanding basic financial measures will help you avoid serious investment mistakes.

Experiment With Dummy, Mock, Virtual, or Fake Portfolios -- several companies offer free dummy trading portfolio platforms to help you step gently into stock investing without risking your money.

Choose an Appropriate Online Broker (Offering Custodial Accounts) -- online brokers with no fees and no minimum are ideal.

Avoid Scams-- stay away from penny stocks or anyone who promises returns that are too good to be true.

Investing When You are Almost Broke

As I mentioned earlier, one of the main obstacles for teens interested in investing is having the cash to do so. However, this problem for most teen investors has started to disappear because you can now start investing with as little as $1. That’s right — financial innovation in the stock market allows investors very little money because you can now buy a fraction of a share, as you will learn later in this article. But teens who want to invest in the stock market are not going to find investing only $1 appealing.

So, let’s explore other ways to get money for investing in stocks. If you have a job — whether it is money for chores around the house or money from an actual job — you can set aside money periodically to invest in the stock market.

However, if you are not fortunate enough to generate a source of cash for investing in the stock market, you need to find other ways to get money.

If you are lucky enough to get a regular allowance from your parents, you can allocate a piece of it for investing in the stock market. You can even ask them to increase the allowance amount so that you can put the increased amount into stocks.

Grandparents are always keen to encourage financial responsibility amongst their grandkids, so you can start your money-raising campaign with them.

If you have relatives that periodically give you cash gifts, let them know that you intend to put some of that money into stocks. Signaling your intentions may even encourage them to provide you with more if they know you are responsible with the money.

If you find that you still don’t have enough money to invest or any money at all, don’t fret. You can still learn the basics of investing with dummy portfolios which I’ll discuss later.

Custodial Accounts for Teen Investors

How old do you have to be to invest in stocks on your own? If you are under 18, you cannot own stocks, mutual funds, and other financial assets outright. As a minor, you can make investments only under the supervision of your parent (or an adult) through a custodial account. Your parent will have to sign you up for a custodial account offered by an online broker.

Without boring you with unnecessary details, all you have to know is that two types of custodial accounts are used for establishing investment accounts for anyone considered a minor (i.e., under 18).

One account is established under the Uniform Gift to Minors Act (UGMA); and

The other account is established under the Uniform Transfer to Minors Act (UTMA).

Either one of these accounts would allow your parents to give you money so you can buy stocks or other assets (under their supervision). Which type you open will largely depend on the state in which you reside.

You would own the assets in the custodial account, but your parent would control the investments in it (hopefully, with your help) until you are no longer a minor. Important considerations in choosing a custodial online trading account include:

Looking for no stock trading fees – you should find online brokers charging $0 to buy and sell stocks.

Looking for low-balance stock trading accounts – make sure the online broker does not require you to maintain a sizeable minimum balance in a trading account; many offer $0 minimum balance.

Looking for brokers that allow you to buy fractional shares – if you want to invest as little as $1 in reputable companies with high stock prices, you can only do so if the online broker allows you to buy fractions of a share of stock.

Choice of Online Brokers for Teen Investors

It has never been easier for teens to invest in stocks and other financial assets. Financial innovations by online brokers such as no-fee stock trading, the ability to buy fractional shares, and well-designed investment apps have made it easier for teens like you to become investors. (Please see our homepage for more information about the important articles and tools featured in this site to help teens become investors).

Here are some online brokers you and your parents may want to investigate as candidates for suitable custodial accounts:

Some of the companies on this list, such as Greenlightcard and Bloom, are relatively new and were established to serve teen investors and their parents. They have investing apps that make it easy to open investment accounts for teens and for these teens to invest in stocks with their parents’ approval. One of the older companies on this list, Fidelity, started a new program a couple of years ago called the Fidelity Youth Account, which made a big splash in the press when it was launched. This program provided an easy way for kids to invest in stocks. However, parents need a regular Fidelity account to register their children for the account.

You may notice that one very prominent online broker, Robinhood, is missing from this list. There is a very good reason for this — the company did not offer custodial accounts at the time of the writing.

Buying Individual Shares of Stock

If you want to buy individual stocks, thousands of stocks are listed on US stock exchanges. Researching each of these companies is an impossible task. It is probably wiser to begin by looking at big companies such as those found in an index like the Dow Jones Industrial Average (the Dow) if you want to buy individual stocks. In addition, some aspiring teen investors begin by choosing stocks with which they are familiar. I discuss these options in the two sections below.

The Dow Stocks

The Dow is an index that gives you a general idea of the health of the overall stock market. It consists of 30 companies, some of which you may already know, such as Verizon, Nike, McDonalds, Microsoft, Coca-Cola, etc. I have included a link to the companies in the Dow so you can see the rest of the big companies in the index and the stock symbols you would need to find out more about the companies.

Most of the share prices of the companies in the Dow will fall in the range of $50-$500. Even if you want to invest less money, for example, $5, you can do so through online brokers that allow you to buy fractional shares, as I discussed earlier.

If you buy individual stocks, it becomes even more important to learn the basics of stock investing. Without an understanding of investing fundamentals, you risk quickly losing whatever little money you cobble to start building your nest egg.

Stocks of Companies You Already Know

If the stocks in the Dow don’t interest you, you may want to look into stocks of companies that teens like. A company called Piper Sandler does a survey each year of over 7,000 teens to discover what brands they like and use. These include brands of shoe companies, restaurants, snacks, clothing, and many other consumer items and services young people use. Basing stock purchases on brand recognition may not be the best way to decide what stocks to buy, but the companies in the survey may give you some initial investment ideas. Later, when you get more experienced in investing, you can do fundamental research to see which stocks are worth your money.

Here is a list of some of the top brands that may be of interest to teen investors:

Top 3 Footwear Brands: Nike (Nike, Inc.), Converse (Nike, Inc.), Vans (VF Corporation)

Top 3 Handbag Brands: Coach (Tapestry, Inc.), Michael Kors (Capri Holdings), Kate Spade (Tapestry, Inc.)

Top 3 Restaurants: Chipotle (Chipotle Mexican Grill, Inc.), Starbucks (Starbucks Corporation), McDonald’s (McDonald's Corporation)

Top 3 Snacks: Goldfish (Campbell Soup Company), Lays (PepsiCo, Inc.), Cheez-it (Kellogg Company)

Top 3 Clothing Brands: Nike (Nike, Inc.), American Eagle (American Eagle Outfitters, Inc.), Lululemon (Lululemon Athletica Inc.)

Top 3 Payment Apps: Apple Pay (Apple, Inc.), Cash App (Block, Inc.), PayPal (PayPal Holdings, Inc.)

Getting Information about Stocks

As a starting point, you should get a copy of the company's annual report in which you may want to invest. An annual report is a document most public companies use to disclose corporate information to their stockholders yearly. It is usually a state-of-the-company report, including an opening letter from the Chief Executive Officer, financial data, results of operations, market segment information, new product plans, subsidiary activities, and research and development activities on future programs.

You can get any company's annual report with a quick google search. For example, if you want the annual report for Nike, enter "Nike annual report" in a Google dialog box. I did such a search and ended up on a Nike website page with all of the company's annual reports.

You can get other information about any company, such as the company's stock symbol (which is necessary for trading stock) and stock price from Yahoo!Finance (finance.yahoo.com). For example, if you type Nike in the dialog box of the Yahoo!Finance landing page, you will see information about NKE – Nike's stock symbol.

It is not always obvious what company makes any particular product just by its name. So you'll have to do a simple search on the Internet to get the name of companies that make your favorite products. For example, the companies that make Goldfish snacks, Lays potato chips, and Cheez-it are the Campbell Soup Company, PePsico Inc., and the Kellog Company, respectively, as shown in the list of favorite teen brands above.

Using a Mock Portfolio to Practice Investing in Stocks

In an earlier section, I discussed the fact that most teen investors don’t have much money to invest in stocks even if they can spend as little as $1 to buy fractions of shares. If you find yourself in this situation, there are a few sites that will allow you to set up a mock stock portfolio and trade stocks with virtual dollars. With these sites, you can play with stocks without risking any money but you will start to learn how the stock market moves up and down. More importantly, it will show you that investing in stocks is not a way to get rich quickly.

With these mock portfolio sites, you can set up a dummy portfolio and the site will tally up the value of your stocks on a daily basis so you can see how the value of your portfolio moves on a daily basis. The websites use real trading data from US stock exchanges to tabulate the value of the portfolios. To set up your own dummy stock portfolio, you’d normally have to join a “stock market game on the site or set up your own game (if the site allows it).

For example, we have our own free portal called TeenVestor Mock Portfolios which we designed especially for teen investors. The portal has a stock game called the Dow-Only Competition which allows anyone to create a portfolio of Dow companies.

Other mock portfolio portals include: MarketWatch Virtual Stock Exchange, Wall Street Survivor, and How the Market Works.

Before you can create your own dummy portfolio with TeenVestor Mock Portfolios, you have to join one of the stock competitions we’ve created within the game’s platform. Each competition has its rules and regulations about what type of stocks you can buy, the amount of initial virtual cash you can play with, etc.

Investing in an Index-Based Exchange Traded Fund (ETF)

As a teen investor, you probably want to reduce the risk in your initial investments. Buying one share of stock, even if it is the stock of a big company, may still put your money at risk.

However, Exchange Traded Funds (ETFs) are investments that represent a diversified group of companies that trade just like stocks. ETFs have been around since about 1993, which is a short time for an investment product, but they have been highly successful in attracting investors who want to reduce the risk they take in buying stocks.

Index-Based ETFs

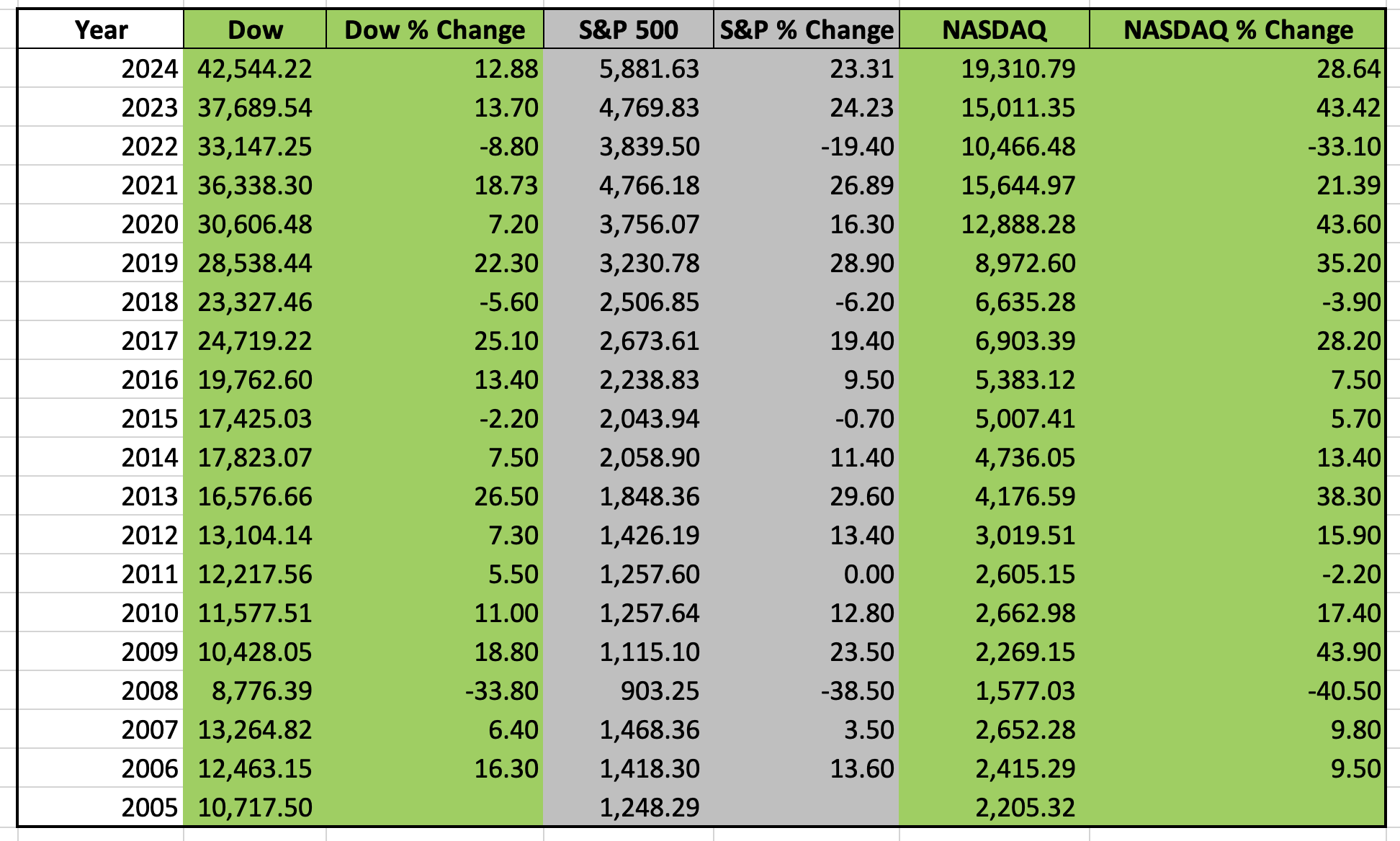

Most ETFs trading in the marketplace are index-based. An index, as explained here, is used to gauge the movement of the broad market. Some index-based ETFs seek to deliver the same return as the major US indexes like the Dow, the S&P 500, and the NASDAQ (further described in the linked page) as shown in the table below.

The Value of the Dow, the S&P 500, and the NASDAQ

Returns of Index-Based ETFs

Let’s assume you invested in an index-based ETF that tracked the Dow on the last day of 2023. Your return by the end of 2024 would have been about 12.88% as shown in the table (in the “% of Change” column for the Dow for 2024).

Returns can fluctuate from year-to-year, however. For example, if you’d invested $100 in an ETF index that tracked the Dow at the end of 2007, your $100 investment would have lost you about $33.80 (or -33.8% as shown in the table in the “% of Change” column for the Dow for 2008) by the end of 2008.

Over an extended period, however, the overall return of an index ETF based on the Dow would be positive. So even if the value of an index-based ETF goes down, it will rebound in the long run. The advantage of being young is that when it comes to investing, time is your friend.

ETF Symbols

To get any information about ETFs, you will need their symbols. The symbols for ETFs associated with the three popular indexes is shown below:

The Dow ETF: SPDR Dow Jones Industrial Average ETF Trust - symbol: DIA

The S&P 500: Vanguard S&P 500 ETF - symbol VOO

The NASDAQ: Invesco QQQ - symbol: QQQ

Getting Information about ETFs

Once you have the symbol of an ETF, what do you do with it?

With the symbol, you can get the price of a share of an ETF just as you can with stocks, as I will discuss in the next section.

I use the financial website Yahoo!Finance (www.finance.yahoo.com) to get the price of the ETFs shown in the prior section. Once you enter the website, type the symbols in the dialog box. Here are the prices for three index-based ETFs as of the beginning of 2024:

The Dow ETF Price Per Share (symbol DIA): $376.9;

The S&P 500 ETF Price Per Share (symbol VOO): $436.8

The NASDAQ ETF Price Per Share (symbol QQQ): $409.5

If you don’t have this kind of money to invest in whole shares of index-based ETFs, you can buy a fractional share if the online broker you chose will allow you to do so.

Buy US Saving Bonds

Savings bonds are loans American citizens make to the U.S. government. Savings bonds can only be viewed as a way to save money, not necessarily a way to earn much interest.

Two Types of U.S. Savings Bonds

There are two types of savings bonds: Series EE U.S. Savings Bonds (or Series EE Bonds) and Series I Savings Bonds. Both types of bonds are low-risk investments that pay interest for up to 30 years.

The U.S. Treasury stopped issuing paper savings bonds – you merely register to buy the securities at the website, www.treasurydirect.gov. Like any other investment, a minor will need a parent or guardian to open up a custodial account in their name.

Series EE Bonds

You are promised a specific fixed interest rate over 30 years with Series EE Bonds. The U.S. Treasury announces the interest rates for new Series EE Bonds each year on May 1 and November 1.

At the time of this writing, the interest rate you would earn on a Series EE Bond is a measly 0.10% per year.

You have to invest at least $25 in a Series EE Bond, but you cannot invest more than $10,000 each calendar year. You can only cash in the bond after one year or more. However, if you cash in the bond before five years, you will lose some interest. When you cash in the bond, or it matures, you will receive the accumulated interest minus penalties for early redemptions, if any.

Series I Savings Bonds

The Series I Savings Bonds are similar to the Series EE Bonds with one crucial distinction: the Series I Bond interest rate is adjusted periodically based on the inflation rate. Specifically, the interest rate is based on a formula, which adds a fixed interest rate, and a rate related to the CPI-U inflation rate. At the time of this writing, the annual interest rate you would earn in the I Savings Bonds is 1.06%.

Certificate of Deposits (CDs)

Checking, savings, or money market deposit accounts are great places to keep money you may need within days. But if you don't need all your money right away, you may want to put some of it into a Certificate of Deposit (CD).

Here are a couple of important things you need to know about a CD:

It offers a guaranteed interest rate for a period of time. CDs usually offer a guaranteed rate of interest for a specified time period, such as six months or one year. Once you choose the term, the bank will generally require that you keep your money in the account until the term ends (for example, until maturity).

It offers higher rates than other bank deposits. Because you agree to leave your funds in the account for a specified period of time, the institution will generally pay you a higher rate of interest than it would for a savings, checking, or money market deposit account.

Interest Rate of CDs

The interest rates you will get for investing in a CD will increase depending on the investment term. For example, at the time of this writing, online bank Ally Bank offers the following CD rates for different terms: 3-month CD at 0.50%; 6-month CD at 0.75% annual rate; 1-year CD at 1.75% annual rate; and 5-year CD at 2.75% annual rate.

Granted, these rates are pretty low, but that is because we are currently living in a relatively low-interest rate environment even though interest rates are starting to climb because of inflation. By contrast, the 3-month CD rate in December of 1980 (when inflation was shockingly high) was about 18.7%.

The highest CD rates can be found at online banks and credit unions. When you shop for CD rates, make sure that the bank does not have a minimum required deposit or any fees.

At the very least, a CD will force you to put money away, which you can’t withdraw on a whim.